- World of DaaS

- Posts

- Morning Consult CEO Michael Ramlet

Morning Consult CEO Michael Ramlet

AI, Consumer Sentiment and Reinventing Survey Research

|  |  |

Michael Ramlet is the co-founder and CEO of Morning Consult, a global decision intelligence company that runs 30,000 daily interviews across 40 countries. The company works with the Fed, Fortune 500s, and a quarter of the Global 2000 to track public opinion and economic sentiment in real time.

In this episode of World of DaaS, Michael and Auren discuss:

Why traditional polling broke and what comes next

How to build high-frequency, global survey infrastructure

What it really takes to get a representative sample

The growing gap in global trust toward AI

1. The Evolution and Disruption of Survey Research

Michael Ramlet, CEO of Morning Consult, describes how polling has changed over time, from door-to-door interviews to online and mobile formats. Legacy polling companies struggled to adjust, especially when it came to sourcing representative samples in global markets. Morning Consult’s early breakthrough was pricing survey respondents based on difficulty of acquisition, similar to a commodities model. This allowed them to scale efficiently and collect more precise, targeted data.

2. Real-Time Data and the Rise of Nowcasting

Ramlet highlights the value of high-frequency survey data compared to traditional methods like the Michigan Consumer Sentiment Index. By conducting 30,000 daily interviews, Morning Consult offers real-time insights that institutions like the Federal Reserve now rely on. Their approach combines survey data with transaction data to create more predictive indicators. This has helped decision-makers benchmark consumer behavior and sentiment ahead of actual market movements.

3. Representation and Global Sentiment Gaps

Getting a representative sample is one of the hardest challenges in polling, especially when predicting who will actually participate in political events. Ramlet notes that consumer sentiment is no longer uniform. It now varies widely by geography, income, and other factors. He also observes global differences in attitudes toward AI, with developing countries showing more optimism than wealthier nations like the United States, which tends to approach AI with more skepticism and concern.

4. Building Differently and Breaking Norms

Morning Consult started in Washington, D.C., and operated without venture capital for its first five years. Ramlet says not following the typical Silicon Valley playbook gave the company more time to mature and focus on long-term goals. He challenges the conventional wisdom that startups must raise from blue-chip VCs or be based in the Bay Area. For data-driven businesses, he argues that having the right strategic location and capital alignment matters more than chasing hype.

“You can’t go back in time to collect data. So we committed to collecting it every day, even before we had customers for it.”

“Instead of 600 interviews a month like legacy polls, we’re doing 6,000 a day in the U.S. and 24,000 more around the world.”

“The difference between weak-kneed leaders and strong ones is knowing where the data is…and still making the right decision, even if it’s unpopular.”

The full transcript of the podcast can be found below:

Auren Hoffman (@auren) (00:01.006) Hello fellow data nerds my guest today is Michael Ramlet. Michael is the co-founder and CEO of Morning Consult, a global survey research and decision intelligence company. He started the company in 2014. It has grown to over a hundred million in revenue and Morning Consult now conducts over 30,000 interviews every day across 40 countries. Michael, welcome to World of DaaS. I'm very excited. Now, where's like, why did you like traditional

Michael Ramlet (00:24.318) Thank you for having me.

Auren Hoffman (@auren) (00:30.574) just break out.

Michael Ramlet (00:32.584) I think you have to think about polling more broadly in a historical context. So it's gone through mode shifts in the past. You go back to the Roman census and I guess all the way to today's census, they're still knocking on doors and doing live in-person interviews. The next big sort of mode shift was to mail-based surveys. And then you get a mode shift to telephone. And then you've now got this most recent shift online and essentially from desktop to mobile. And so I think you think about each one of those

Components and the parts of it are different. Just think about from the labor cost standpoint, the cost of a survey if you're doing live telephone or in person is really the cost of the person's time conducting the interview. That's very different in a mobile and online world when there's not a live human being conducting it. And so I think what it takes to be good at any one of those modes is very different. And most of the legacy players started in a live telephone or a live in-person world. And so they had no choice.

Auren Hoffman (@auren) (01:28.558) when I was when I was in high school, and this is like, you know, hundreds of years ago, I used to like, fill out these surveys, and then they would send me like 10 bucks for filling out the survey. And I loved I just constantly filling out surveys. And I just try to make as much money as possible doing it. But also, it was like fun to fill out the surveys and stuff like, and that was like, you know, and that was the day that was, yeah, that was the is, you know, that was in the mail physical mail, I would send it back.

Michael Ramlet (01:47.294) Yeah. You don't do it for the incentive.

Yeah. Yeah. Yeah. Think about it this way, right? Like who's, it's a real problem with the time, value and money if you're doing it to make a living. And we ask a lot of psychographics about the motivations of taking surveys. And I think the two things that stand out are there's a lot of folks that don't necessarily have a job or a role in their family, in which they make a lot of decisions. So I they find it empowering to sort of share their opinion. think secondly, you know, not every job is a highly engaging intellectual exercise. And so I think other folks find it intellectually stimulating.

Auren Hoffman (@auren) (02:15.789) Yep.

Michael Ramlet (02:23.37) And I think those tend to be more so the case, especially among older respondents or among respondents who are of higher incomes.

Auren Hoffman (@auren) (02:29.742) Well, people like answering questions about themselves, right? Like they love that. Like, I mean, you could, cause you felt like those personality tests online are super popular. Like what kind of cat are you or something? Right? So people love that stuff.

Michael Ramlet (02:44.042) But it speaks to how hard it is to go find a representative sample. And that's been the big failure of the legacy players is that they just didn't take the time to understand what it takes to be successful from a supply chain standpoint. It's harder to find a representative sample than randomly calling the phone book. lot easier to run a polling operation where you just randomly dial the phone book. Much harder to go find representative samples, not just in the US, but certainly abroad, especially in developing markets. And I think that's a big challenge that the industry.

Auren Hoffman (@auren) (02:48.246) Yes, okay.

Michael Ramlet (03:11.882) legacy players just didn't care to focus on a lot of it. They were going through the private equity turnstiles. So the idea of investing in kind of what was a cost center for the industry, I think held it back. Everything that happened in ad tech over last 20, 25 years just didn't happen in the survey market research industry.

Auren Hoffman (@auren) (03:27.2) And often like once you start, the end is pretty small. So once you start like subdividing the end, even if the end is like 1200 people, well, once you sort of saying, okay, well, this age group and this gender and this state and this, you know, all of a sudden the end could be like five people or something, right?

Michael Ramlet (03:44.618) Well, that's the problem, right? With live telephone in person, it is extremely expensive. I think one of the things that was our first big unlock and flexion moment was when we realized that people were not differentiating by how difficult it was to get that survey responded. There are more women in the Western Census region between 18 and 29 willing to take a survey and make them between 50 and 100K, than there are over 65 men without a high school degree living in the Midwest. You should pay more for those men and less for those women. And that was the first big unlock for us. Essentially, at our core,

We're like a commodities trading hedge fund. We're better at acquiring a higher quality interview, but because you can drive down the unit costs through those bidding algorithms, now all of sudden you can do these much larger sample sizes. So to your point before, like the big frustration point was like, once you got to a second demographic or a subgeography, you had very small sample sizes. And that was always the Achilles heel of these large telephone operations. You just couldn't get enough respondents. The other part is like, you can't show visuals. You can't do other.

Auren Hoffman (@auren) (04:38.263) Yeah.

Michael Ramlet (04:42.27) sort of dynamic tests in an audible telephone call. And it takes longer to actually read the interview than it would be to read the screen.

Auren Hoffman (@auren) (04:50.35) There's also like a spot poll or spot questionnaire where you want to figure something out. But then sometimes you want to ask the same group of people over time similar questions and see how those people are evolving as well. And there you don't want you it's really important you don't have or you have as little churn as possible in that poll, I presume, right?

Michael Ramlet (05:14.314) Yeah, I if you think about it from our perspective, some of us we got lucky. So, you know, I think we had good ideas and we thought we were going work really hard, but you know, right time, right place. We got to start the business and cloud-based computing world when everyone else had on-premise servers in the industry. think we looked at it and said we wanted to go every day because our whole mission was we wanted real-time intelligence on what people think around the world. And from our standpoint, I mean, you had to constantly be asking them what they think. And so to your point, kind of a set

standard questionnaire that goes every day. So it's kind of 30,000 interviews, no matter what we're going to go and collect the data. But what became the lucky part of that was because we had guaranteed demand, you could have peaks and troughs for other surveys that are going on. So the supply chain really loved us because we could guarantee an extremely large volume. And in exchange with the bidding algorithms, we were essentially able to achieve most favored nation status. So we drove down the unit cost.

while actually increasing the volume of surveys that the supply chain can expect. And those things allowed us to get smarter and smarter around what it costs to get what population in what country. And so it became this reinforcing network effect.

Auren Hoffman (@auren) (06:22.99) No, you have like the Bureau of Labor Statistics, like traditionally and like called people up or called employers up or called HR departments up. And I know they still do that. Right. But then there's also like real data that they see, like they can like, you know, I think they get data from ADP. They get some other data that they actually like in some ways that's like passive. That's almost like a passive survey, you know, where they're getting the real like, well, how do you think about that? Because obviously you can get data of like.

Michael Ramlet (06:31.312) Still do to be clear.

Auren Hoffman (@auren) (06:50.048) Are you still using Netflix? But you could also get the credit card data as well, which would prove if they're actually like getting billed by Netflix or if they're turning from Netflix to Disney plus or something like that.

Michael Ramlet (07:01.962) Yeah, I think it's a combination of both worlds, right? Like you're thinking about it before you do it. So the tighter that timeframe, like if it's an impulse purchase at the convenience store counter, like the transaction data is probably going to be extremely accurate because it happens at the frequency. The even better idea is like just the tier to which some of those CBG companies don't have that point of sale data point and have it processed instantaneously. And so I think when we look at it, a good example would be the work we do at the Chicago Fed for their carts model, they're pulling in

Auren Hoffman (@auren) (07:15.8) Yep.

Michael Ramlet (07:30.794) the large data processor, credit card transaction data, and then they're marrying it with the survey-based outlook data on consumer and retail spending. So I think from our standpoint, we really try to benchmark against what would be the sort of real world outcomes. So the normal thing we do is we benchmark, for instance, against equity markets. On a platform called Meet in Century, they'll do all the back testing for all of our brand indicators. You might be thinking about taking that vacation weeks before you actually...

make the transaction on Airbnb or another booking platform. And so subsequently, that's a two to three week alpha that you might be able to leverage out of that database and then to be able to benchmark it against the underlying SEC reportable financials. think we've seen that as the sweet spot of behavioral data married with that real time sentiment, representative survey data.

Auren Hoffman (@auren) (08:18.158) In some ways, like if you think of data companies are often like doing one of two things and it seems like you're doing both. One is they're trying, they're trying desperately to predict the past and really trying to get an accurate position of what happened in the past. And then there's other companies that are trying to predict the future. And they're both actually incredibly difficult to do. Right. So you can have, you you can have, Hey, what do you feel about this? But you can also, Hey, are you going to make a purchase in the future or something as well? Right.

Michael Ramlet (08:46.954) Well, that's where it comes back to the frequency part of it. You look at the Michigan Consumer Summit Index, it's great that it goes back to the 40s. It's deeply problematic that it's at best like 600, 700 people. It takes three weeks to process the data. So by the time they're reporting the data publicly, that was our big unlock at the beginning of the pandemic was we had gone to the Fed and said, hey, we're doing instead of like 600 a month, we're 6,000 a day in the US. And then, oh, by the way, we translated 24,000 interviews.

in those 43 international markets, it's programmatically available in API at like 1 a.m. East Coast time. And that was a big demonstration of credibility and capability. What we originally approached the central banks about was are there other indicators like inflation at that point, you really hadn't seen any meaningful inflation, so there's a lot of discussion about should the market basket change. And so we actually started working with the central banks around like what are new potential indicators given kind of the gray economy and the gig economy writ large.

And what then happened at the beginning of the pandemic, the feds cited, you know, came back to say, hey, remember that daily data you're talking to us about? Can we get that? And, I think to the surprise of all our large banking clients who use the brand tracking capabilities, it was like, wait, you have daily data on consumer sentiment in the US. I think for us up until that point, you just didn't have the like, my gosh, I needed this moment to make a decision right now. And I think that has sped up since the pandemic.

Auren Hoffman (@auren) (10:08.418) Yeah. And the Fed is a big consumer. mean, we're involved with so many data companies and a large portion of those sell data to the Fed. So the Fed is a very big buyer of different types of stuff. If they find it like an interesting data set, they're willing to buy it and see if that can be predictive or help them understand like a nuanced thing.

Michael Ramlet (10:29.514) I think the approach that go on now casting is that right middle ground, like the challenge of predicting the future, like so many like insert favorite like quote. But I think that now casting ability of like, here's the accurate barometer of higher frequency data at this moment in time. And I think that's what you're seeing, as I'm seeing from CEO CFOs, they're pulling guidance because the ability to sort of give that confident guidance nine, 12 months out, but they still have to get on the earnings call and talk about what happened in the last quarter and what do they expect in the next quarter.

And so that sort of now casting capability, to your point, the fed's been a pioneer in, I think that's where we're seeing some of most sophisticated activity.

Auren Hoffman (@auren) (11:06.988) And there was this, if you remember, there was this study of Harvard students that JFK was actually in that study and a lot of famous people and they kind of like, it was a 60 plus year study.

where they actually followed these students and they would follow surveys of them and they saw how they changed over time. But of course it was just very narrow, like super elite, know, mostly super wealthy back then, all men back pretty back then study there. And yeah, they have all these findings from this, but it was just, again, so narrow, like

What would you, if you could like reimagine in something like that in today's world, where we're going to, you know, what is that? Do we get their medical records? Do we get like their bank statements? Do we get like, do we get their like Fitbit and like Apple watch readings on a daily basis? Some of these, you know, like how could we reimagine something like that today?

Michael Ramlet (12:08.97) I mean, we think a lot about how challenging it is to get a representative sample of a population to get the data off of. And so think we felt really lucky. We also played with a little bit of house money. We bootstrapped the first five years. So there wasn't much parental supervision. And I think in hindsight, that was to our benefit because the idea of committing to going to do that many interviews on a daily basis really committed to a high fixed cost. But the reality was if we could sell it and stay ahead of that curve, then we could continue to expand the data set.

And so I think from our standpoint, we were excited because the thing we knew you couldn't do is go back in time and collect the data. And the representativeness of what you could do with surveys was the really valuable kind of...

Auren Hoffman (@auren) (12:46.296) But with some data you can, mean, like there are some data sets that are like, you actually can go back in time and get payroll data. can go back in time and get, you know, so there are these data sets, are like somewhat substitutes for surveys as well.

Michael Ramlet (12:53.176) totally!

Michael Ramlet (13:00.362) And you get really limited demographics off of it. I think that's what we were always excited about. I think when we look at our data set, what makes it different is the breadth of the data. If we think about every row is a person, every column is a question, and you can cut every column on another column. And so think from our standpoint, where we look at other numerical data sets, and I think what made it challenging from an engineering standpoint was just how

Auren Hoffman (@auren) (13:05.431) Yeah.

Michael Ramlet (13:26.952) the breadth of the database is a little bit different than some of really large numerical data sets. And I think that was really.

Auren Hoffman (@auren) (13:31.982) Like, you know, if you think of like Rod, so Rod Chetty, know, he's an economist at Harvard. He's got access to the IRS data. So he, you know, which is this like massive study on over a hundred million Americans, their kids, their grandkids, how are they doing? How do people change? How much do they give to charity? How much do they move around? I mean, it's just incredible study that, that

like maybe four or five researchers in the world get access to, maybe unfairly, right? Like, could you imagine if like, everyone could get access to that again, like in in a, in a, in a anonymous way, like it could really blow out the, the, the world's knowledge or something.

Michael Ramlet (14:04.17) Yeah, there's like more- yeah, exactly.

Michael Ramlet (14:16.104) Yeah, but it's still confined to what they ask the questions on, right? I think that's always like, when we look at it as like this desire to ask anything we possibly could want in the future to try and get even more breadth. So like, for instance, like one of my greatest regrets is like, I wish we had tracked the housing market sooner. Like it just would have been even more compelling to have a larger longitudinal database to it. But I think, you know, obviously you have to make, you know, gives and takes when you have the capital to make those investments. But I think from our standpoint,

Auren Hoffman (@auren) (14:19.224) Sure. Yeah.

Auren Hoffman (@auren) (14:38.732) Yep.

Michael Ramlet (14:46.078) the issue is, know, or the exciting thing was we could keep adding to it. And that, you know, obviously the investment in some of these large longitudinal studies at a governmental level has dissipated or they're locked into a mode. Like I think that was the challenge for Michigan was just they had always done it telephonically and they just didn't make the jumps. They made the jump a year ago and all of a sudden the trends all break and it's a lot more challenging for them to find a representative sample online than what they thought was sort of representative sample.

on telephone and you see this then in terms of market movements, you had some pretty wild swings in the first three months of this year with that monthly data set. think that's the innovators element of core, right? Like you're gonna have some mode effects. That's what keeps me up at night is like, okay, is there a mode effect change that takes place?

Auren Hoffman (@auren) (15:31.766) having like representative samples always heard like even the SMP 500, right? It's like that, that, those 500 companies are very different than the 500 companies that were there 50 years ago in the same index. And so they have to like slowly add, they have to slowly reweight. have to think about all the, like it's, I mean, it's very nuanced and very hard. And of course, like everyone hates it. Everyone thinks it's stupid, right? Everyone argues with it.

Michael Ramlet (15:58.09) And everyone wants to be in it for higher trading.

Auren Hoffman (@auren) (15:59.776) Yeah, of course. Everyone wants to be in it. Of course. Yeah. so, I mean, I think these things are really hard to like get any type of sample that people will believe, cause it's, it's always like a religious battle. when you're, when you're talking about a sample.

Michael Ramlet (16:13.482) Yeah, I think if you had like the synopsis of what went wrong in the survey market, because it's a way bigger industry than most people realize. know, Andreessen wrote a note a couple of weeks ago that pegs at 140 billion. You know, the number I tend to look at on at least the quantitative size around 80, 90 billion. So there's plenty of money being spent in category. is extremely fragmented. So I think that's one of the things that oftentimes surprises me. 100%. Yeah. And also there wasn't economies of scale around the tech stack.

Auren Hoffman (@auren) (16:35.746) And survey could just be like one expert too sometimes, right? Yeah.

Michael Ramlet (16:43.432) And so think if you looked at like what was the problem, the industry was too slow in terms of the frequency and processing of the data. it wasn't getting large enough sample sizes to do that kind of second, third level, common to Horel look. And then the third was just too expensive. Like it just was prohibitively expensive to go and collect that data. And I think that's what's exciting now about where the industry is like a lot of those things I think have been unlocked. You you still have the legacy pieces of it. The big question will be for survey research.

you know, what is the next evolution of it look like in terms of not just traditionally survey data in the context of political polling, but in the context of economic data, there's a lot of pressure, especially on even developed economies at this point, to find representative samples. then frankly, even more so the case in market research, kind of like corporate capacity.

Auren Hoffman (@auren) (17:31.884) Now the market itself in some ways is a massive survey where people actually put their dollars. if you, you know, the, the, market that, you know, the, market about the Apple stock price is actually like a very efficient market, that's out there. So, and then of course, now we have these like prediction markets where people are trying to opine on tons of different things. And those tend to be really interesting and, you know, quite predictive as well. Like, how do you think about like the markets in general?

Michael Ramlet (18:00.872) I think at our core, want to be a leading indicator of any market. regardless of whether it's betting markets on a particular event or if it's equity markets or if it's currency markets, because obviously tracking a lot of the underlying economic sentiment pieces globally plays into the currency effects play. But I think from our standpoint, those markets reflect all.

Auren Hoffman (@auren) (18:20.408) Sure, not necessarily from your ship, but how do you think about just in general, these prediction markets? What do you like about these markets? What do you?

Michael Ramlet (18:24.296) Yeah.

Michael Ramlet (18:28.552) I think making markets creates transparency and I think that's a good thing. So I don't think there's any downside. I the question is like what's informing that market activity. And what you saw in like political prediction markets is that surveys were being used throughout that process. So even like the whale on that kind of larger Harris Trump bet like, you know, was conducting his own private surveys. So I think the degree to which like it's going to inform markets, I think our view is that the more market making that's going on, the more opportunities there are leverage the data.

Auren Hoffman (@auren) (18:42.158) Of course. Yeah.

Michael Ramlet (18:58.708) So I think we're pretty proud of the development.

Auren Hoffman (@auren) (19:00.982) And what is stopping, you know, some of these mongrels still like not, there's, you know, a lot of Americans can't bet on them, et cetera. So there's like less liquidity than there could be in these and maybe, maybe it's less accurate because of that. Or I don't know. How do you think about that?

Michael Ramlet (19:18.474) I think it's the breadth of things that you'll want to track go beyond what the markets cover. So like they tend to be very like event driven markets and maybe things like 100 % in terms of like, yeah, yeah. Yeah. the X amount of rainfall in like, yeah, all that kind of like IBKR. Totally. But that like, I think is why I don't.

Auren Hoffman (@auren) (19:27.79) Yeah. Well, they tend to be things you can easily adjudicate. right. So it has to be, you know, will the Fed increase, you know, 0.25 % or not by this date? Yeah. Yeah. Yeah. Then it's easy. If there's a nuance, it's hard to, hard to bet on it. Right.

Michael Ramlet (19:47.95) I don't view them as replacing. think it's a way to monetize that type of knowledge and to really hone in. think there's just such a broader use case of the data. Understanding your customer base isn't going to be derived out of prediction markets or understanding the...

Auren Hoffman (@auren) (19:49.879) Yeah.

Michael Ramlet (20:10.346) A good example might be like, what is the underlying interest among a emerging population in a particular product? Like one of my favorite, like, when did we have the early data? And I wish we had our own hedge fund was like, you could see the effect of the Bad Bunny Post Malone sponsorships on croc sales, like six weeks ahead of like reported earnings. Just this like massive pop in the daily tracking around interest from Gen Z and then from Gen Z's parents.

Auren Hoffman (@auren) (20:17.71) Yep.

Michael Ramlet (20:39.978) And you could see it in the data. and you could specifically like, did the bad bunny like sponsorship drop and what did the Post Malone sponsorship drop? And you're like, man, I wish we could trade on that like type of information. it gets as colorful as, you know, hasn't been something we tracked so much on this. We get so much non-public information that I don't trade, but it definitely, we have a bunch of buy side clients, but the question on those are like,

Auren Hoffman (@auren) (20:52.182) Is Croc a public company? I don't even know. Yeah. Yeah. Yeah. Yeah.

Yeah.

Auren Hoffman (@auren) (21:06.488) you, you personally don't trade because of the information or...

Michael Ramlet (21:09.82) No, yeah, we have, you over a quarter of the global 2000 are clients. And so I think we're constantly exposed to non-public information. I think Congress should take the same position, you know, we'll see. Yeah. So I think from our standpoint, we really feel like prediction markets are additive. I think in the same way that we're really excited about building a benchmark against equity, know, benchmarks against currency benchmarks, those things create opportunities for real world comparison and improve the process.

Auren Hoffman (@auren) (21:17.272) Got it, so you just find it safer not to trade at all? Yeah.

Michael Ramlet (21:39.102) The political polling is really hard. And I think this is not fully understood. It's not about finding a representative sample of US, because it's not compulsory voting, not everyone votes. And the issue is every election cycle, whether it's a midterm or presidential, has an entirely different participation composition. And so you have to both predict who's likely going to show up and you then have to go find a representative sample of that prediction. And so think that's why it's like the ultimate test. Yeah.

Auren Hoffman (@auren) (22:03.566) Yep. It's like a double, double problem. Yeah. Yeah.

Michael Ramlet (22:07.676) It's an incredibly challenging proposition. think, you know, if you're running a business, you're probably not looking to win.

Auren Hoffman (@auren) (22:13.58) And also like, like there are some things that, you know, maybe the president, like everyone in the country has an opinion on, but basically after the president, like you go down just one more level, like a lot of people don't even know who their governor is. Right. It's like, it's like a really hard, it's really hard to like, like pull on like these like lower information types of things.

Michael Ramlet (22:37.418) Yeah, I think you got to think about like, is the activity? If you're running a political campaign, you're running all the way through election day. So you're looking at lot of the momentum shifts and the tactics and whether it's working or it's not. I think you're looking at it from a business standpoint, like you're not trying to win the product category like 48, 47. Like hopefully you're trying to win it by a much larger margin. And I think what folks misunderstand is that like the data gives you a context of where it is today. It doesn't mean that's guaranteed where it will be tomorrow. Obviously like the shorter term prediction, like the more accuracy.

Auren Hoffman (@auren) (22:54.124) Yep.

Michael Ramlet (23:07.338) But the issue is that you can move public opinion. I think that's the thing that differentiates really great executives, really great political leaders. It just gives you a sense of how much you're going to have to educate or persuade and move a larger population. And I think that's the difference between weak-kneed leaders and leaders with conviction is, hey, I understand where the data is. This is the right decision to go in that direction. But I recognize in the short-term, the onus is on me to provide that education or...

know, hold steady for those numbers to materialize over the intermediate long-term.

Auren Hoffman (@auren) (23:38.382) If you look at like the last president's erase Trump Harris, it did seem like a lot of the Trump ads were about persuading people. were finding niche audiences, black men or whatever niche they could find. And then even maybe more niche than that. then trying to persuade them to move. And if they could just get X amount moving like that would lead. And of course, they're only

Trying to persuade people in the seven or eight states that mattered and stuff where it seemed like the Harris was like much more broader. Just trying to like, maybe get people out to vote or, you know, they were, they were advertising in states that they didn't like, how do you, when you kind of, know you're not a political person, but how do you, how do you break down their strategies?

Michael Ramlet (24:25.844) Yeah, I think from our standpoint, obviously make the full API available. So you can take advantage of the like six plus million interviews we do in the U S and you can see like the dramatic events like Biden's debate or stepping out of debate. And you obviously see like, you know, anything within the margins within the margin. That's what kind of is incredible about like how tight the most recent cycles have been. I think what stands out to me is like kind of the way you describe it, which is like.

Auren Hoffman (@auren) (24:37.708) Yeah.

Michael Ramlet (24:50.6) the political aspect of spending money in this space is even more aggressive on an even tighter timeline than what large corporations do. Like they're essentially standing up like a full scale multi like national company overnight in like three, six months. They're moving a billion dollars. And so just the degree to what, and yes, there are like appendages and all the different pieces, but the reality is like you're essentially scaffolding on the fly at, you know,

Auren Hoffman (@auren) (25:06.41) Yeah, yeah, yeah, yeah.

Michael Ramlet (25:19.978) outside of open AI, very rare levels of like that level of like growth in terms of like the scale of an operation. And I think from Mars, well, we're surprised by, and I think this also surprised me folks in the political spaces, for how advanced the ad tech side of it is, the polling and like research side of it, like these are predominantly a small group of still a lot of just predominantly men in the DC area that have been doing it for 20, 30 years.

Auren Hoffman (@auren) (25:44.438) Yeah, a lot of them are super old. Yeah. Yeah.

Michael Ramlet (25:46.91) They own their own call center. They'll send you a physical binder. You walk into any major campaign office and there's a wall money.

Auren Hoffman (@auren) (25:53.452) I mean, I know a lot of them and these guys like they like, like a bunch of them, like went to Harvard in the seventies and they're like super smart. You know, they were the first like the people to think about data in the seventies and stuff like that. But like, they're still the guys who are pulling, like, it's just crazy that it's like, it hasn't really evolved. Yeah.

Michael Ramlet (26:11.614) But at that point, it's more about like you're this trusted strategist than you are like it's a data driven operation. I think that's where the differentiation really splits between like larger corporate applications or financial service applications versus political applications. Like it gives you a read on that. I think that'll change. Like at some point here, it evolves. think my, when we first started, because we started the company out of DC and a lot of us had different backgrounds. And just a joke, like the old school pollsters couldn't program anything other than a nest.

Auren Hoffman (@auren) (26:17.856) Yeah, good point. Yeah.

Michael Ramlet (26:40.714) And I think like the degree to which like.

Auren Hoffman (@auren) (26:42.958) Well, by the way, I don't think that's true. think a lot of them actually were like, they, were good programmers for their day. Yeah. Yeah. Yeah. They actually could, they actually, you know, they certainly could write good SQL and they could do, you know, they could write like they had, they had, you know, but they were, they still, they kind of came out of that like seventies. Like they were the first ones, the reason why they were successful. They were the first people to adopt computers. Like if you read the histories of all these like pollsters, like who started in the seventies, they're amazing. Yeah. Yeah. Yeah.

Michael Ramlet (26:48.81) Yeah, so, like, the larger sets of, like, not belly-length, they're not base-form, like... Yeah, and...

Michael Ramlet (27:08.638) Yeah, yeah. Kenny ends up running the overnight like mayoral races and totally like, but the reality is like for how long like that, it's been the same way for political polling for two or three decades. One of the reasons why we never went into this space. The other is it's just not a particularly good business model to follow. think from our standpoint, what we wanted to do was to benchmark daily datasets against the toughest challenges. And one of which is how do you track politics? I think, you know, if you look at the modern political polling space today, I think we take a lot of credit for

we forced everyone to have to move to daily. That was never something that was an expectation. All your old school media partnerships once a month at best 600, 800 responses. If you look at it in the last five years, I think this was starting to change too. It's not just about US politics. It's not just about US politics in the context of US politics. So for instance, like those 24,000 interviews that we do a day in 42 international markets, like you can see the impact of

Auren Hoffman (@auren) (27:39.906) Yeah.

Auren Hoffman (@auren) (27:45.997) Yep.

Michael Ramlet (28:06.122) American politics around the globe. You can see, for instance, geopolitical risk implications. China in the lead up to the tariff announcements beginning with kind of the North American tariff announcements. China passes the US and global net favorability for the first time ever in our tracking, presumably for the first time post World War II. And you you see the US dynamic playing out internationally. You obviously had about 75 percent of the world's population. Right.

Auren Hoffman (@auren) (28:08.344) Sure.

Auren Hoffman (@auren) (28:31.746) Yeah, which is super worrisome. Yeah.

Michael Ramlet (28:34.442) 100 % in terms of like the expectation. think that general America is like, America has this really, you know, legitimate goodwill in foreign markets. That's not the case. The bricks, obviously, most recently with kind of their announcement on visas.

Auren Hoffman (@auren) (28:45.774) When we think about, let's say, consumer sentiment, how is like the tech industry doing in consumer? You hear about things where the consumers are becoming more anti-tech, but then you also hear the most, maybe the companies that are most admired in the world are companies like Apple and Amazon and Google. So where is that going?

Michael Ramlet (29:09.499) It's like Congress. People hate Congress, they like their Congress person. And like even like in this era of like unprecedented disruption, like still like 90 some percent of them get reelected, but like Congress approval rate never lowered. I think the interesting dynamic on this is actually developing.

Auren Hoffman (@auren) (29:12.632) huh. Yeah. Yeah.

Auren Hoffman (@auren) (29:18.956) Yeah, exactly. Yeah.

Auren Hoffman (@auren) (29:24.354) And by the way, I don't know that they like their congressman, they just don't like the other person running against their congressman. Yeah, yeah, yeah, yeah, yeah. Yes, I don't know they have any true love for their congressperson. Yeah.

Michael Ramlet (29:29.002) Yeah, like all kinds of like, yeah, I just think the general thing is like, I hate Congress, but yet like the average Congress person gets really like to extraordinarily high clip. I think what's interesting to me is this distinction between established economies and developing economies. And you see a 30 point percentage gap between developing economies and developing countries, you know, over 50 % plus like net favorability towards AI.

and you've got, or trust in technology and AI and in established economies, you've got 20 % in decline.

Auren Hoffman (@auren) (30:04.28) We were using developing it's even more pro AI.

Michael Ramlet (30:07.322) A higher level of trust, higher level of like...

Auren Hoffman (@auren) (30:10.19) Oh, I wouldn't have thought that. wouldn't have, I would have thought they would, they would be in some ways like they might be the first guys on the chopping block who get, who get, who get hit by it. Like I think AI is going to hurt, hurt India and the Philippines much faster than it will hurt Germany and America or something.

Michael Ramlet (30:20.05) Possibly, but in terms of making sure...

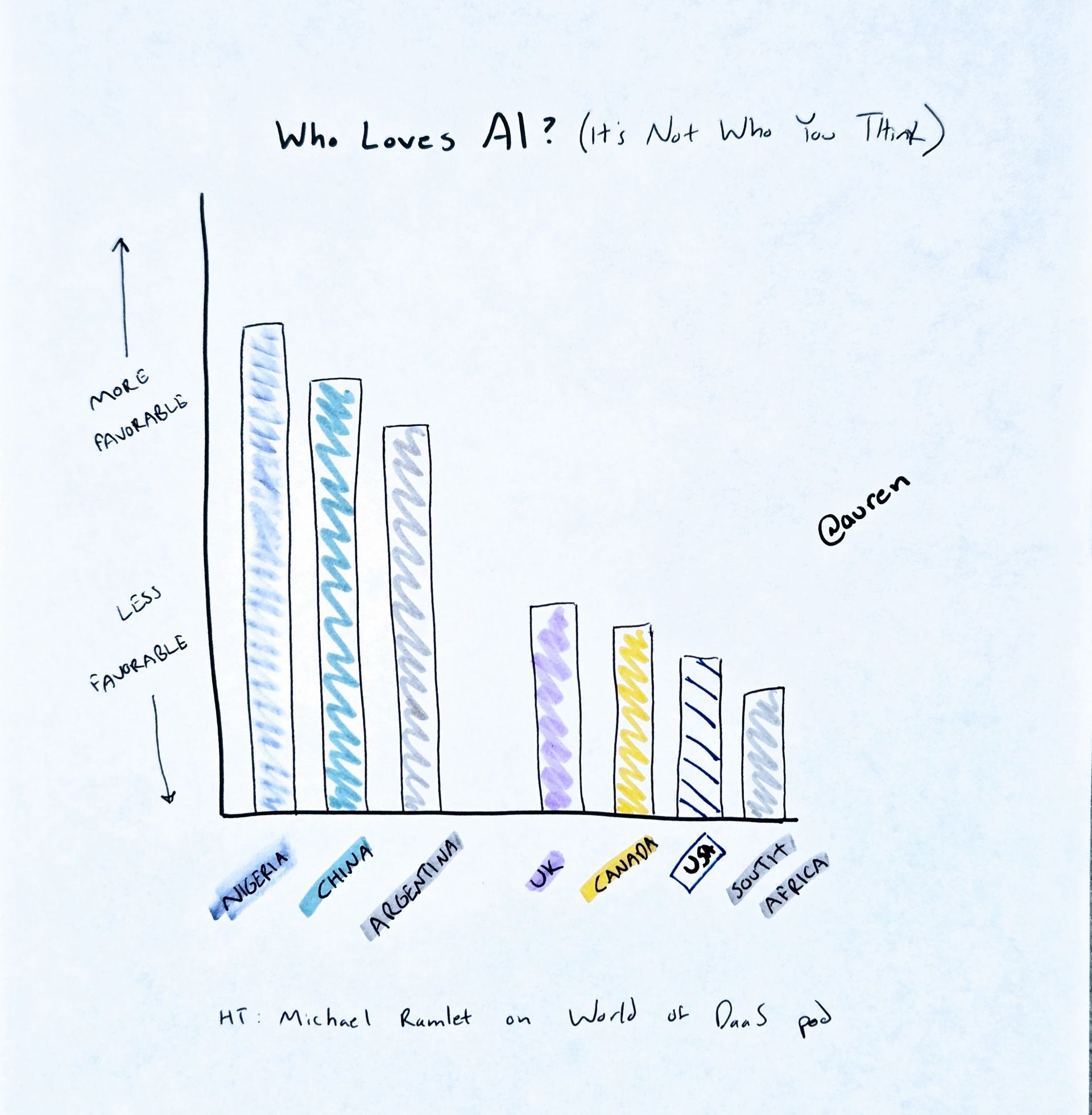

Michael Ramlet (30:27.732) And it's not like, obviously it's not always the case that the public thinks something that's necessarily reflected in the numbers. Yeah, I think from our standpoint, probably the thing that stands out the most in terms of favorability or kind of outlook in general feel towards AI, the second most favorable outlook among the G20 is among China. The second worst outlook is among the US. And so you see this very significant Nigeria.

Auren Hoffman (@auren) (30:31.598) Correct. Yeah.

Auren Hoffman (@auren) (30:48.766) Wow. Who's most favorable in the G20? interesting. I would have not thought that. Yeah.

Michael Ramlet (30:56.958) Yeah, because most favorable goes Nigeria, China, Argentina. The least favorable South Africa, US, Canada, UK, and fourth least favorite.

Auren Hoffman (@auren) (31:06.646) interesting.

Interesting. Okay. What's your psychological profile of the US's why the US is 19th out of 20 in favorability toward AI and what's your psychological profile of China where there are two out of 20?

Michael Ramlet (31:10.731) Presumably, there's some aspects of it.

Michael Ramlet (31:19.05) I mean,

Michael Ramlet (31:23.678) Presumably there's some aspect, well, some of it's also information dissemination. I don't know what, obviously, in Chinese market.

Auren Hoffman (@auren) (31:28.055) Yeah.

Auren Hoffman (@auren) (31:31.734) Yeah, I step on like a scary boogeyman and stuff like that. Yeah

Michael Ramlet (31:35.176) Yeah, and obviously too, I think this degree to which a lot of the largest, most developed economies, they have the most to lose in terms of the average economic participant. And so I think that probably has a factor into the kind fear gauge aspect.

Auren Hoffman (@auren) (31:50.883) As you're seeing other like interesting consumer trends, what other trends would you think are interesting that are happening or things that were people were excited about and now they're less excited or vice versa?

Michael Ramlet (32:03.53) I think the number one thing is the degree to which consumer sentiment has been fragmented and just the underlying health of the consumer. So I think in the past you had like sort of those national metrics around like, here is the U.S. consumer sentiment. And the issue is that it is fractured dramatically around income ones. You see some reporting on that, but it's even more dramatic if you're in like the QSR space right now, or you're in casual dining or you're in fast food. Like the difference between going to the higher end of that spectrum

Auren Hoffman (@auren) (32:17.101) Yeah.

Michael Ramlet (32:32.85) and down, like middle-income consumers look much more like lower-income consumers. I think you see it by geography. So like the housing market, that's what I saying before, like my bigger grads I wish we had our housing data going back further. Cause you can see that in certain cities, the housing dynamic, like I feel a wealthier if I'm in a stronger housing market, if I own a home, than necessarily what I may be doing in a market that's in a more significant contraction. So I think it's just the fragmentation of it. Like you had more...

Auren Hoffman (@auren) (32:51.566) Yeah.

Auren Hoffman (@auren) (33:00.034) How does housing like play, because America is a weird country where it's, you know, very high percentage home ownership. It's, it's, you know, let's say the reverse of Germany, which is very low home ownership, even though also like a relatively wealthy country that's out there. Like, I don't know, I don't know the facts, but maybe US is the highest in the, one of the highest in the world in terms of home ownership.

Michael Ramlet (33:21.034) Yeah. Take a second step onto that dynamic. The US also uses fixed year more or fixed income or fixed interest rate mortgages. That's not the case in the UK.

Auren Hoffman (@auren) (33:28.238) Yeah, which is very, very, that's right. It's very pro consumer to just lock that lock that 30 year mortgage in at that a few percent.

Michael Ramlet (33:35.914) Right. And so that's, that's what I think like the markets, you know, in this sort of going on, I guess, like 18 months of like sort of recessionary calls, the bears, like it just, if you locked in a 2 % mortgage rate, you're changing homes because you're not going to get a 2 % rate today, but you feel pretty good about the rise in home value. And that gives you some economic boost or sentiment boost and you're going out and spending. And so that's why I think when we look at like,

Auren Hoffman (@auren) (33:48.974) Yeah, you're sitting pretty. Yeah.

Auren Hoffman (@auren) (34:03.906) Yeah. By the way, like, I don't even understand, like, imagine if you have a variable mortgage rate and so, you know, imagine like every month, if you're like, you know, if your rent was changing every month, you would just go crazy. And especially if it like doubled, like over a six month period, right? You would go crazy.

Michael Ramlet (34:13.312) yeah.

Michael Ramlet (34:20.852) Well, they to be shorter, they tend to be shorter duration too. So it's like an even larger swing.

Auren Hoffman (@auren) (34:25.535) Yeah. Yeah. Like, I don't know, I don't know how you deal with that. I understand why so few people own homes because they probably have to just like, they probably have to put way more in cash because getting a loan is pretty scary if it's going to change all the time. Whereas in the U S like you only have to put 20 % down or something. It's a lot more easy to afford something.

Michael Ramlet (34:45.716) And I think that's the most sophisticated use case that I've seen here this year is the degree to which you're seeing now those CFOs be able to tease out customer bases. And we're seeing it from sell side research, we're seeing it from buy side. It's not like how is the housing market or home improvement market? The CEO of Home Depot broke this out on their earnings call with our data. And it was what specifically the sentiment of the Home Depot customer base and how is that similar or different to the competitive set?

Auren Hoffman (@auren) (35:11.288) Yep.

Michael Ramlet (35:13.61) So I think it's leveling the kind of regional or subpopulation dynamics. It's almost, and this is why AI is so exciting.

Auren Hoffman (@auren) (35:22.326) Home Depot might be more concentrated in the Southeast of America and it might be more, you know, male dominant or whatever it might be.

Michael Ramlet (35:30.92) Yeah, there are all the different components of it, but the idea is that like essentially in the past you had to go off these national metrics. And then I think the hardest thing, this is what I'm excited about with AI applications is just like, it's telling people to ask the question. Cause I think one of the hardest things is like the technical limitations of what was possible for meant that you had a closed minded understanding of what you could ask for. It's like, like I, they told me I couldn't ask for Atlanta based data, you know, cause it didn't exist 10, 15 years ago. I think that's the aspect of it that gets.

Auren Hoffman (@auren) (35:55.192) Yeah.

Michael Ramlet (36:00.282) It's problematic, I think, for older executives in particular. And I think it's just the degree to which you have to stay open-minded. I mean, know this across, obviously, the world of DAS. The assets that are coming online are so dramatically expansive compared to what they were even 10, 15 years ago.

Auren Hoffman (@auren) (36:17.528) How are consumers adopting it? Like when I, when I talk to a 20 year old, it seems like a hundred percent of them are using some sort of AI tool on a daily basis. They're a daily active user. When I talk to a 50 year old, it's, it's very rare. And when I talk to a seven year old, it's like super rare.

that they're using any of these tools. I'll tell you, maybe a couple of them are like have AI in the background or something like a Duolingo or something, but they're not actually like using them as much. is it that, am I right? Is it that bifurcated?

Michael Ramlet (36:49.908) Well, don't recognize that they're using them because they might be using Google search and they're starting to get like the tech. Right. 100%.

Auren Hoffman (@auren) (36:54.446) That's right. That's right. They might, but I'm saying they're not like actively thinking they're benefiting from AI or it's like the 20 year old is like actively going to, you know, perplexity or chat GPT or anthropic or, or Gemini or something. And they're, they're like actively engaging and asking questions.

Michael Ramlet (37:11.274) February, 2023, we asked US adults. So this doesn't have the age breakout, but they've got to follow up. Just 2 % of US adults in February, 2023 said they use chat GPT several times a day. As of April of 2025, that number was 14%. So 600 % increase in terms of multiple daily use cases in the population. And so my guess is that it would follow a similar but accelerated, like I would look towards out of our data set, like what was the adoption curve for TikTok?

Auren Hoffman (@auren) (37:15.81) Yeah.

Auren Hoffman (@auren) (37:28.471) Yep.

Auren Hoffman (@auren) (37:32.942) It's very concentrated in the younger people. Yeah.

Michael Ramlet (37:41.034) or what was the adoption curve for like Instagram? Like TikTok's great, cause I can see it in the full 10 year like data set, like the advent of it. And then like what are those tipping point moments where all of a sudden it goes from like it's a Gen Z thing to a millennial thing to a boomer.

Auren Hoffman (@auren) (37:46.605) Yep.

Auren Hoffman (@auren) (37:54.254) Yeah. Yeah. Cause I was, I just came from a family gathering and I was like, I was surprised at how little the adults there were using. I wasn't surprised that the 20 year olds were using it. Uh, cause like if you're in college, you have, you have to use, like it's kind of like, it's necessary even in high school, like it's necessary to be using these tools. will not.

you would be lapped very quickly if you're not using those tools. But I was surprised like really that they were like everybody was like AI curious. These are smart people, my family, but they were like their usage was quite low.

Michael Ramlet (38:30.218) So this is something we think is a huge opportunity, especially the older executives or established executives is they might be afraid to send like the analyst an email asking for data point, but in the like quasi like anonymity of AI, you can ask wherever you want. There's no like, you know, there's no reputational. It's like, you know, think there's a number of like, I think we look at the AI application for our data.

Auren Hoffman (@auren) (38:46.646) Yeah, totally. That's the randomest thing. Yeah, yeah.

Michael Ramlet (38:56.75) as democratizing access. Before it was very much analytical functions or insights, analytics. They might have the raw API. They might use the SAS platform. But with the tool, I think it opens up the ability for more more executives to ask questions. They might be afraid of asking another team. Sure.

Auren Hoffman (@auren) (39:14.968) How are you personally not not how is your company but how are you Michael Ramlet using AI personally?

Michael Ramlet (39:21.13) I think on a daily basis, the ability to use AI to come up with really compelling things for kids. So I have a six-year-old, a four-year-old, and an 18-month-old. So you can come up with obviously all kinds of different bedtime stories. Yeah, the creative side of that.

Auren Hoffman (@auren) (39:28.184) Yeah.

Auren Hoffman (@auren) (39:33.144) Stories and stuff like that and you're actually doing it like I mean I keep hearing about people doing it But like you're actually like getting getting cool stories and stuff Characters yeah Yeah, that's kind of cool. Yeah

Michael Ramlet (39:39.13) No, think that's always like really trying to figure out like ways and like that's like one aspect of it. I think that the way I still use it the most is for business like questions, right? Like it's just incorrect. I have an obsession with all of our code names are 20th century Industrial Revolution like names. So like literally the books, like it's the Titans, the House of Morgan type like naming conventions. And so instead of having to like think about how to explain why we went with this code name, it's like.

Auren Hoffman (@auren) (39:58.539) huh.

Michael Ramlet (40:06.986) We have an operation Bessemer. it's like asking AI, like, up a summary of the Bessemer press and how it transforms like steel and the civilization of America. That's a much, yeah. It's not really like my day to day job, but like, yeah, you come across something and it's just a little bit more compelling to go back through. So I think on a personal basis, more than like the history.

Auren Hoffman (@auren) (40:10.243) Yeah.

Auren Hoffman (@auren) (40:14.712) Yep.

Auren Hoffman (@auren) (40:19.763) It's kind of fine. Yeah. Yeah.

Auren Hoffman (@auren) (40:27.756) And where, where do you, when you're personally using it, where do you see like that kind of like a physical frontier where you're, where there's a limitation that you see, but you're like confident in the next six or 12 months, it's going to kind of like, you're going to be able to use it for that.

Michael Ramlet (40:45.002) I mean, I think about it in professional setting for me personally is just right now, for instance, like we have the capability of asking like kind of a jobs to be done analysis before I go into any pitch or any client meeting. And it will pull up all of the sort of publicly available information, but then it will cross it with all of our underlying data assets. And so I think, you know, what does that mean in terms of the, we're trying to talk about it in the context of like, don't think about like where it's going to be in six, 12, 18 months. Like you don't know that definitive answer.

Auren Hoffman (@auren) (41:03.84) Internal. Yep.

Michael Ramlet (41:14.954) think about what would be the best possible end destination and just assume at some point between now and then there's an inflection moment that makes that possible. And so I think, you when we look at it as like a lot of those things require some multi-step like pieces to it. The reality is like agents like should be able to at some point in the not too distant future, like that the equity prep or the earnings prep pack that we should be able to send to you should be entirely automated like from start to finish and it should look and feel differently.

It's not like in automation, just replicating the same report every time, you know, eight, 10 weeks before your public earnings call, you should be getting a generated earnings prep pack from the platform. And I think those things like all of it gets tighter and it's less of like the multi-step piece to it or less of like sort of the human in the loop review component to it. I think that's where like, I see the biggest change for us, but I also think that's true of like most businesses, like how many people are in that support function.

putting together like that earnings prep pack that all of a sudden now, like whether it's operational data, whether it's public opinion data, like we're collecting or financial data, like all of those things can be organized and synthesized so much faster. So I look at it, the most recent case that saved me a ton of time was we were building out this outreach campaign to equity research analysts. Cause we're just, we had all the inbound and we're sort of thinking, okay, this is generating it.

The ability to write essentially a prompt that can pull who the equity research analysts are for any given security. You can go find it. You can dig through different finance platforms, but to get it within 15 seconds is magic.

Auren Hoffman (@auren) (42:49.666) Yep.

Auren Hoffman (@auren) (42:57.774) Now you, was, is it a feature or a bug if you go back, you know, 11 years to, you know, found, think founded the company in like DC. Now you're, I believe you're in the Midwest. Like, is there, is there a feature bug that you weren't in the Bay area, the San Francisco Bay area? Yeah.

Michael Ramlet (43:14.868) Well, I don't want jump the gun because I think you guys traditionally ask that, like, what's the conventional wisdom advice that you... Yeah, I didn't want to make the mold. You know, I think the conventional wisdom that's wrong is you have to race from Blue Chip BC. That's the like the core conventional wisdom. And I think that it was probably right during a period of time. Obviously, access to capital is changing and evolving, but I mean it less in the sense of...

Auren Hoffman (@auren) (43:20.32) Yeah, okay, yeah, let's jump the gun. Let's do it. Yeah, yeah, yeah. Yeah, okay, yeah.

Michael Ramlet (43:43.402) It's not the signaling factor of it, because I think you can now go raise money from a lot of places. It's more about the alignment aspect of it. And we got really lucky. We thought we were going to raise around from a fund who one of their partners got indicted the day that the academician scandal broke. And it was the best thing that ever happened to us. We ended up going and raising from three really great non-traditional blue chip VCs. One was Lupus Systems from James Murdock. The other was...

Auren Hoffman (@auren) (44:01.134) Uh-huh.

Michael Ramlet (44:13.514) advanced venture partners from the US family. And the third was the fund out of Susquehanna that it's not in one time limited space. And I think our advantage was that we had all the meetings, we bootstrapped the first five years of the business, but we were out of DC. So that already made us a little weird, especially like pre pandemic. Even though we had kind of the who's who of New York and San Diego road, I think from our standpoint, the biggest thing was this flexibility of like longer duration investing.

Auren Hoffman (@auren) (44:31.202) Yeah.

Michael Ramlet (44:42.6) Like we were not a great like you know, three to five like three to five year bet, because we had to go build the data asset.

Auren Hoffman (@auren) (44:50.03) most venturers are, it's like a, it's like a 10 year plus bet on something usually, right? Yeah.

Michael Ramlet (44:55.518) Yeah, I just meant that like in terms of like, so like from the where we're based type dynamic, it was like, it didn't matter at that point, because we weren't, you know, there was sort of that at least pre pandemic much more stronger feeling of we need to be in the Bay and those pieces. think DC was unique for I was in DC, my national expansion strategy was to move to Chicago within 15 minutes of my mother-in-law and 30 minutes to O'Hare. I can make a lot more East and West coast flights. have a co-founder in New York and a co-founder and still in DC. Our headquarters in DC.

Auren Hoffman (@auren) (45:03.979) Yep.

Michael Ramlet (45:23.786) But like this DC DNA was compelling for our field because you had this familiarity with economic data, with political data. You had all these underlying knowledge bases around survey research. So it was a natural hub and still is the headquarters and probably about 40, 45 % of staff are there. But I think that dynamic, know, the conventional wisdom being like you start a high growth technology startup in the Bay Area, you lose money there.

Auren Hoffman (@auren) (45:48.268) Yeah, and you also like you started bootstrapped in and then kind of raise money, which is also different. Like some people either raise money right away or they'll stay, they'll start bootstrapped and not raise money in the future. Right.

Michael Ramlet (45:58.6) Yeah. Yeah, our big thing was that we got to the point where we could collect the data in the US and then we went through and we thought we were going to do our series A and we found everyone sort of giving a discount to could you collect this data internationally? Because at that point, like you think about like Nielsen, it's like it's predominantly US data set. Like, yes, there are some like international pieces to it, but there wasn't a lot of international data sets in the survey research space like that. And so I think one of things we realized was, you know, we ended up

benefiting from bootstrapping because I think you had to learn the hard thing about hard things. I feel like now I tell everyone it's like, bootstrapping, learn the difference between AR and cash really quickly. And I think the degree to which we benefited from is it gave us time to grow up. I was lucky I had an incredible co-founder. had a data science or research background in counter-op. And then had another technical co-founder, more of the computer science background in Alex Doolin. And for those two guys and myself, it's like it gave us time to

Auren Hoffman (@auren) (46:38.188) Yes.

Michael Ramlet (46:56.414) to get your sea legs and grow up a little bit. think what the value of the capital did was allow us to say, okay, we're gonna start tracking a number of these international markets, even if the client base today is predominantly US centric, it creates the opportunity to sell multinational companies, global assets, and it created the pathways for international expansion down the road, because we knew you'd have to collect the data to then be able to go to market with it. So, know, my...

I think that conventional wisdom, you maybe the YC factor is still real. mean, obviously like the evaluation pieces are there, but I think from our standpoint, especially in these sort of not like defense tech would be another one. They're like, obviously like the DC space has a number of like unique attributes to it. DC I'll tell you is the best.

Auren Hoffman (@auren) (47:36.876) Not really, like if you think of like all the best defense tech companies, mean, very few of them are based in DC. Sure. Of course. Yeah. Eventually they have to have their sales team there. Yeah.

Michael Ramlet (47:40.084) Yeah.

But they have like large DC like bases now. It's a great angel investing community. Cause a lot of folks run lobbying and communication. Like I think for us, like we really benefited from the angel stage on Bootstrap.

Auren Hoffman (@auren) (47:57.262) Yep. All right, since I asked you the last question, asked all of our I'll also I'll ask you now the second to last question we ask all of our guests, which is what is the conspiracy theory that you believe?

Michael Ramlet (48:08.546) so I grew up in Madison, Wisconsin, a Packers, Milwaukee Brewers, Milwaukee Bucks fan.

Auren Hoffman (@auren) (48:12.846) I was just in Wisconsin last week. I love Wisconsin. It's my favorite state, especially in the summer. okay. Yeah. I have a few friends that are shareholders. Yeah.

Michael Ramlet (48:16.808) Wonderful state. That's a Packer Shareholder certificate up there. It's an invitation to the best shareholder meeting. You get drinking tickets to go to the annual meeting at Lambeau. But my conspiracy theory that I do believe, I think is acutely the case in the NBA, is that I think that there is a scripted nature to it. There's certainly a bias towards non-major markets. Good Midwestern, like,

Auren Hoffman (@auren) (48:28.398) Amazing. Yeah.

Michael Ramlet (48:45.448) you look at sort of the finals examples around officiating or the way that players move across the league. Like, I'm all in on a number of the NBA conspiracies.

Auren Hoffman (@auren) (48:54.932) Wait, sorry, I don't even know these NBA conspiracies. Like, give me an example of what's going on there. Yeah.

Michael Ramlet (48:59.514) so it goes back to like you mean in the 85 drafts, like was it orchestrated for the Knicks? You get there's a lot of conspiracies around the Jordan retirement in Chicago. They they covered in the last dance like pretty nauseam. The 2002 Western Conference finals between the Kings and Lakers, just some very like bizarre officiating, unfortunately for Sacramento. So I think, you know, there's a very real bias.

Auren Hoffman (@auren) (49:03.596) Yeah.

Auren Hoffman (@auren) (49:24.526) Oh guys. So you think like the, the NBAs kind of tipping this, they, they tip the scales for the big market teams, like the Lakers, the Celtics, the, mean, I don't know. don't, I don't, as a, as a, as a lifelong Knicks fan, I don't feel like anyone's tipped the scales for the Knicks, but maybe, maybe you're right. Yeah. Like, don't know. Yeah. Yeah. Yeah. Exactly. They've tried, they've tried, but like the odor keeps messing it up. It's like, okay. Yeah. That's fair. Yeah.

Michael Ramlet (49:28.874) Yeah.

I think it's a miracle, Janice still in one.

Michael Ramlet (49:41.61) But now for lack of trying maybe, know, Yeah, I mean, I like there's a good WWE vibe to some of the underlying elements of...

Auren Hoffman (@auren) (49:57.006) Yeah, it does seem like, somehow the Lakers always and the Celtics like always have an amazing team. yeah. Yeah, that's true. Yeah. How did they get that? Like, it's a good point. Like did somebody? Yeah. I, I'm with you. I feel like there's definitely. Yeah. Well, because like, actually, like when you're an owner of a team, you are, it's, it's actually not necessarily in your best interest to have your team do well.

Michael Ramlet (50:01.834) Yeah, you get a crazy trade out of like Dallas.

Michael Ramlet (50:07.918) It surprises everyone in the league. I mean, I'm not saying I agree with everyone. just, feel like...

Auren Hoffman (@auren) (50:26.19) You're, you're really, when you're owner in the NBA or owner in the NFL, you're, you're, you're, you're, you're actually really a, you know, one 28th or whatever owner in the, in the, in the, in the NBA. You really care that the NBA does super well. You don't care about your specific team like the Dallas Mavericks. Right.

Michael Ramlet (50:35.498) Yeah, you're a mess. You're an LP. Yeah. Yeah.

Michael Ramlet (50:44.106) See? There's a lot of incentives to think that there could be some real merit. know, get some referee gambling sagas,

Auren Hoffman (@auren) (50:48.974) Right. Right. It would, it would make sense. Like you just want the NBA to be, to do better, you know, get the bigger contract, the bigger TV contract. Yeah. Yeah. Yeah. By the way, I hate that. I hate the games. They're terrible. I hate watching the games. I don't watch it anymore. They're completely boring. I, I, I have, I, I think they're losing fans. They're just, it's not interesting. Um, I'd love them to like completely change the game, but, uh, so.

Michael Ramlet (50:56.906) Man, and I love the NBA, like I like all the games. I think that there's some real merit to some of it. It's crazy.

Auren Hoffman (@auren) (51:18.188) Yeah, that's my whole stick too. All right. This has been amazing. love, I love this conversation. All the whole conversation we've had. Thank you, Michael Ramlet for joining us. World of DaaS. the way, I follow you at Michael Ramlet on X. definitely encourage our listeners to engage you there. This has been, yeah. Awesome. Okay. Yeah. Do that too. Yeah. People could just like DM you and ask your AI questions. Well, so, this has been amazing. Thanks again for, for coming on.

Michael Ramlet (51:33.096) Yeah, you can access all the data at Morning Consult that I asked everything we talked about today. It's all right there.

Michael Ramlet (51:44.778) Thanks for having me. Take care.

Reply